In the below commentary, we intend to address some of the key considerations and recent developments surrounding the liquidity environment in GP stakes.

Executive Summary

In the following commentary, we intend to address some of the key considerations and recent developments surrounding the liquidity environment in GP stakes:

- GP stakes is a far more liquid asset class than is often perceived

- This perception is largely due both to the youth of the asset class and to its targeted longer hold period

- Forms of monetization are diverse and accelerating:

- 65% of all single-investment liquidity events have happened since 2024

- 44% of all portfolio liquidity events have taken place since 2024

- Continued investor inflows to GP stakes may drive further acceleration of realization activity

GP Stakes Liquidity

One of the first questions a prospective investor typically asks about GP stakes is, “How do you achieve liquidity?” It’s a fair question, but it reflects what we believe to be a common misconception—that the strategy is inherently illiquid in a way other non-control private equity strategies are not. As it pertains to GP stakes investments, while the sample size is small, we believe the success rate for liquidity has been strong in comparison to their targeted holds.

Although we view the notion that GP stakes is an illiquid strategy as a misconception, it persists for several understandable reasons:

- GP stakes is a younger strategy—the oldest fund pursuing private markets GP stakes reached final close in 2016

- Investments in GP stakes have a longer targeted hold period, meaning many investments have not yet matured

- Although the strategy has grown significantly, the number of GP stakes transactions, totaling just over 200, remains limited compared to more traditional strategies, resulting in a smaller sample size

Our team follows GP stakes liquidity events closely and is pleased to provide an update on the trends currently redefining the narrative around liquidity in this market.

In the following commentary, we will address the strategy considerations surrounding liquidity in GP stakes.

Why aren’t there lots of GP stakes exits?

Two key factors have contributed to the limited number of realization events to-date: the youth of the strategy and the longertargeted hold periods.

Private Markets GP Stakes: A Young Market

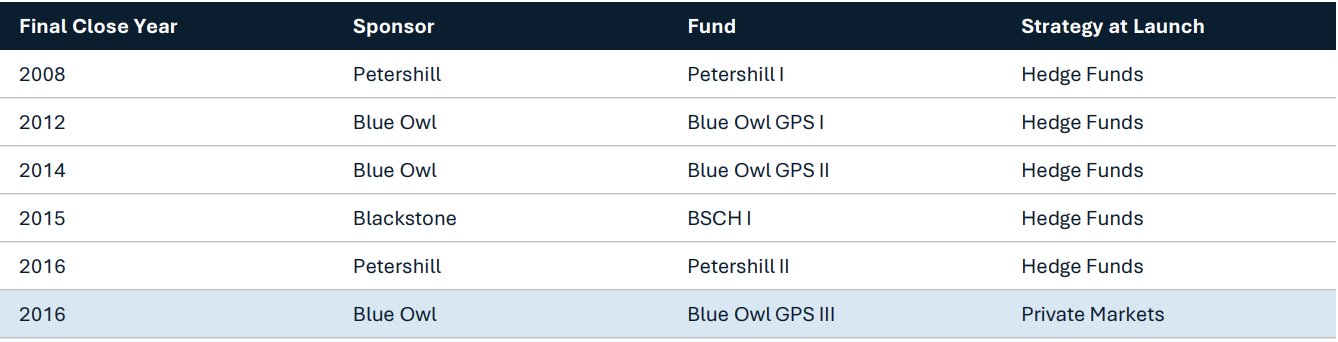

GP stakes investments have existed for decades, dating back to the late 1980’s when Nikko Securities made a strategic investment in Blackstone. Over the late 90’s and early 2000’s, pension plans and sovereign wealth funds completed additional GP stakes investments in many now-prominent firms.

The first GP stakes fund was not launched until 2007 with Petershill I. Unlike GP stakes funds being raised today, this fund was launched with a principal mandate to acquire GP stakes in firms managing hedge funds. This was the approach for materially all GP stakes funds for nearly a decade thereafter.

Figure 1: GP Stakes Fund Preferences at Launch

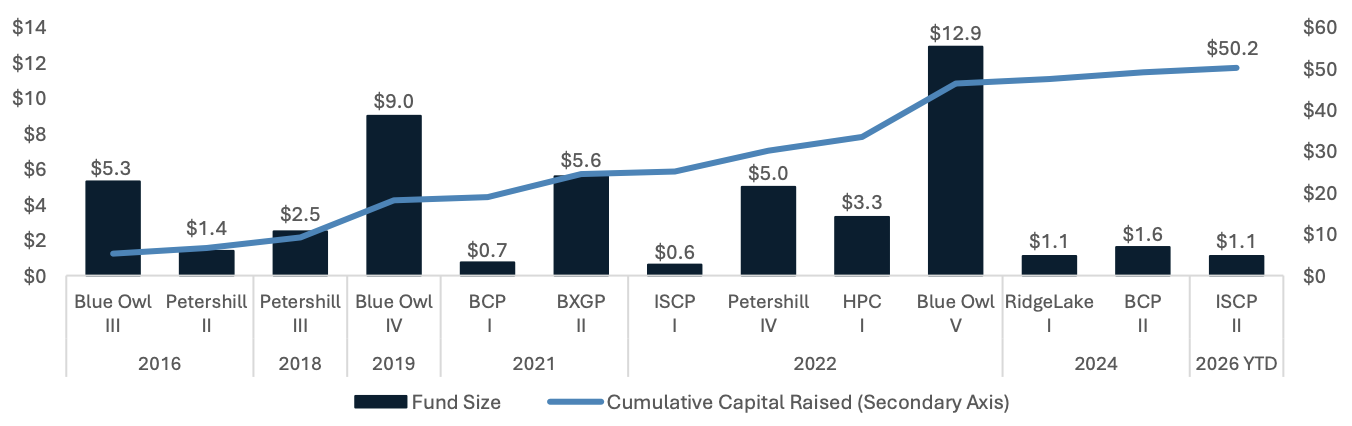

For reasons outlined below, many GP stakes investors underwrite their investments with a 10-year horizon. The oldest GP stakes fund to primarily target private markets, Blue Owl GPS III, is now reaching its 10-year mark. Concurrently, we are beginning to see an acceleration in monetization activity.

Although the oldest private markets focused GP stakes fund is now maturing, the substantial majority of the market is in fact much younger. Numerous sponsors have raised private markets-oriented GP stakes funds and many of these sponsors have successfully raised increasingly larger funds. Since Blue Owl GPS III’s final close in 2016, additional private markets-focused GP stakes funds totaling $45 billion in commitments have closed—representing 9x growth in cumulative capital commitments to the strategy.1

Figure 2: Private Markets-Focused GP Stakes Fundraising Activity ($B)

The weighted average final close vintage of these funds is 2021, making the average fund approximately five years old. Because capital is typically deployed over multiple years, the average underlying GP stakes investment is likely four years old or younger. With an expected hold period of up to ten years, it is therefore unsurprising that most GP stakes investments have yet to reach the stage of ultimate monetization.

GP Stakes Investments Target a Longer Hold Period

GP stakes have a hybrid return objective targeting both private credit levels of yield and private equity levels of appreciation. Over a 10-year investment horizon, the strategy is designed to provide a combination of recurring cash distributions and growth in equity value. The result: strong total returns as portfolios mature and liquidity events materialize.

Each of these objectives—yield and appreciation—require time.

Many GP stakes investors commit to the strategy, in part, for its steady current-income profile. Exiting after only a few years, when investments are just beginning to generate cash flow, would contradict a core objective of the strategy and forgo the opportunity to realize full cash-flow potential.

In addition, equity value in an unlevered GP stakes investment tends to build gradually over time. A successful GP stakes investment does not rely on leverage, inorganic growth, or multiple expansion. As a result, equity appreciation is primarily driven by the organic earnings growth of our sponsors. Organic earnings growth is largely driven by growth in fee-paying AUM (“FPAUM”), which can result from multiple factors, including:

Achieving this level of organic earnings growth takes time for most businesses, irrespective of their model. It tends to be even more time consuming for a GP stakes investment given how GPs generate earnings. Investment performance and realizations may generate yield or have a modest impact on equity value in any given quarter; however, new fund launches are typically the strongest driver of equity value. Many GPs tend to have one dominant product, even when they operate across multiple business lines. A sponsor typically needs to achieve two additional fund launches in their largest product for a GP stakes investor to achieve their target equity appreciation. Assuming a new fund is launched every 3 to 4 years, it would require 6 to 8 years to achieve this milestone.

Forms of Realization

GP stakes portfolios can be realized in two ways: through single-investment realizations or portfolio-level realizations.

Single-Investment Realization

In a single-investment realization, the investor sells its stake in one firm independently of the broader portfolio. This can take multiple forms:

Sale to another GP stakes firm or other financial investor

- Sale to a strategic investor

- Participating in a control sale

- Achieving liquidity in public markets post-IPO

- Sale back to management

Portfolio Realization

In a portfolio realization, the investor assembles a portfolio of GP stakes investments and realizes them collectively. GP stakes investors are able to do this for two reasons:

- Lack of control premium: As a minority investor, GP stakes funds do not pay a control premium. As a result, they can realize full value without selling a minimum proportion of the investment. This flexibility allows them to assemble a targeted portfolio that includes as much (or as little) of each investment as needed to create the most attractive package for buyers and maximize value.

- Portfolio focus: Unlike generalist buyout firms investing across multiple industries and sectors, GP stakes funds invest in one ecosystem. Investors who seek exposure to one high-quality GP often want to own several, provided they meet the same standards.

At the portfolio level, this concentration enables diversification across asset classes, strategies, vintages, sectors, geographies and management teams. Such diversification can reduce risk and stabilize cash flows, creating the potential for multiple expansion.

Portfolio realizations can take multiple shapes as well, including:

- Sale to a larger GP stakes investor

- Sale to a strategic investor including insurance companies, asset managers, or sovereign wealth funds

- Public listing of the fund or portfolio

- Fund-level recapitalization or continuation vehicle

GP Stakes Industry Growth

Figure 3: Estimated GP Stakes and Private Markets Growth

Finally, the LP universe in GP stakes continues to grow and diversify. This runs the gamut from large sovereign wealth funds defining GP stakes as an asset class in their strategic asset allocation, to wealth and retail investors increasing their private markets allocations. There is also emerging interest from secondary investors as GP stakes funds provide similar liquidity characteristics (near-term Distributed to Paid-In (“DPI”), limited J-curve) without the level of price competition often featured in portfolios of primary LP fund commitments.

Not surprisingly, greater capital inflows typically result in a more liquid market. We have seen this in GP stakes with significant acceleration in transaction activity both at the single-investment level and in portfolio realizations.

Transaction Activity: Single-Investment Realizations

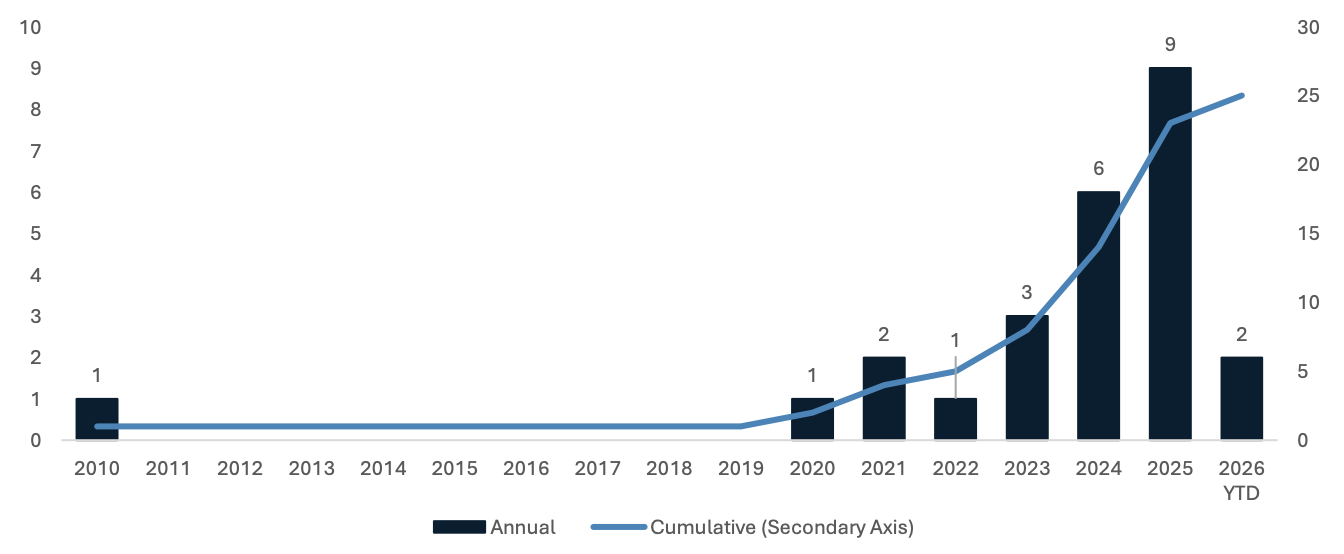

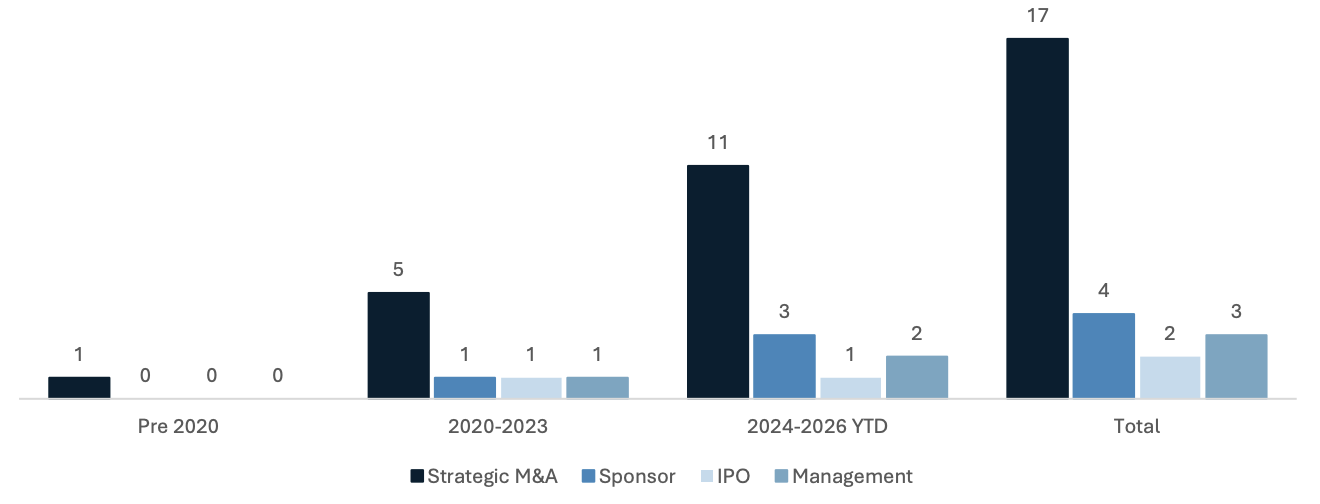

Across programmatic GP stakes investors, there have been 25 single-investment realizations historically. The velocity of these realizations has accelerated. Of these 25 realizations, 24 of them have happened in the last 5 years and 17 have taken place in the last two years. This is a pronounced acceleration.

Figure 4: Single GP Stake Realization Count

Additionally, forms of single stake realizations have become increasingly diverse. Early realizations in GP stakes largely consisted of strategic M&A. While M&A activity continues to rise, other forms of realization have also increased—most notably sponsor-to-sponsor sales.

Figure 5: Single GP Stake Realizations by Type

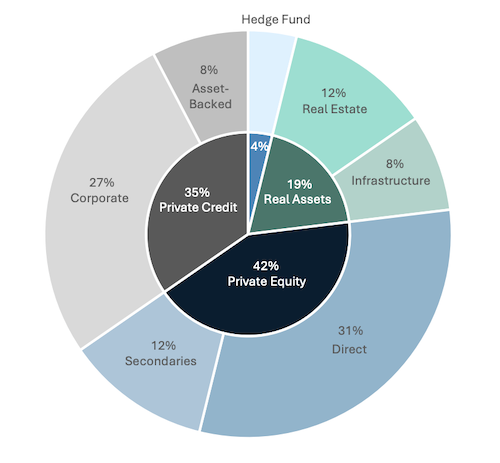

GP stakes investors benefit from the expanding set of single-stake monetization pathways, independent of their investments’ strategies. Historically, realizations have occurred across all market sectors demonstrating exits are accessible throughout the GP stakes universe.

Figure 6: Breakout of Single Stake Monetizations (by Count)

Accelerating Control M&A Activity

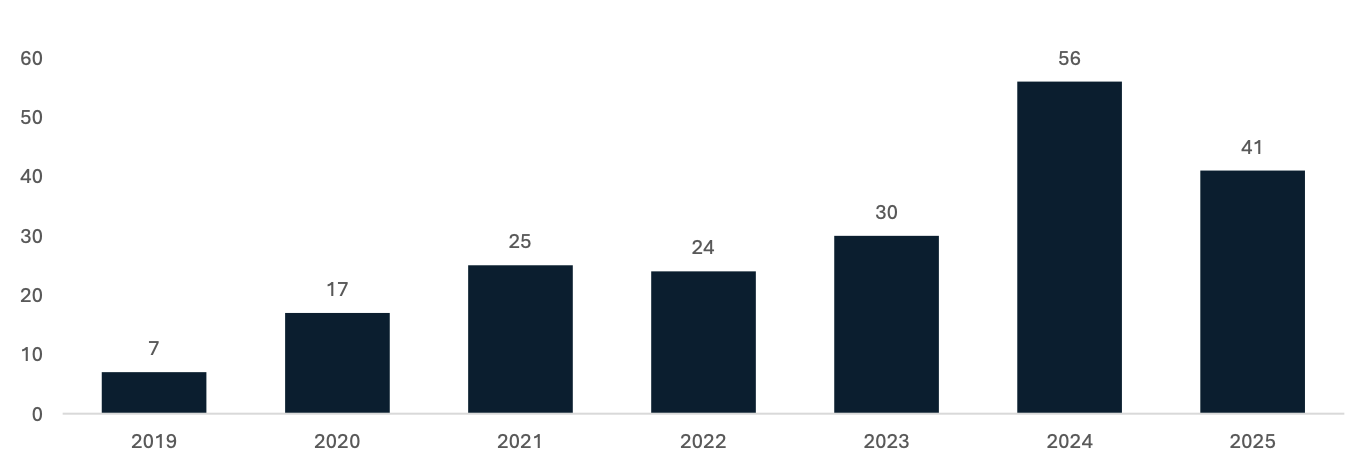

Among the various single-stake exit paths, control acquisitions have been an important and accelerating source of liquidity. Private markets sponsors are in a period of consolidation with M&A activity increasing in recent years. Large private markets sponsors utilize acquisitions to broaden their strategies and expand geographies, while traditional asset managers buy private markets firms to access higher-growth, higher-margin areas. Although deal volume declined in 2025, it remained the second highest year on record for private markets sponsor M&A volume. This level of activity can benefit GP stakes investors as it buoys valuations and provides a path to liquidity for select investments.

Figure 7: Annual Private Markets Sponsor M&A Volume

Transaction Activity: Portfolio Realizations

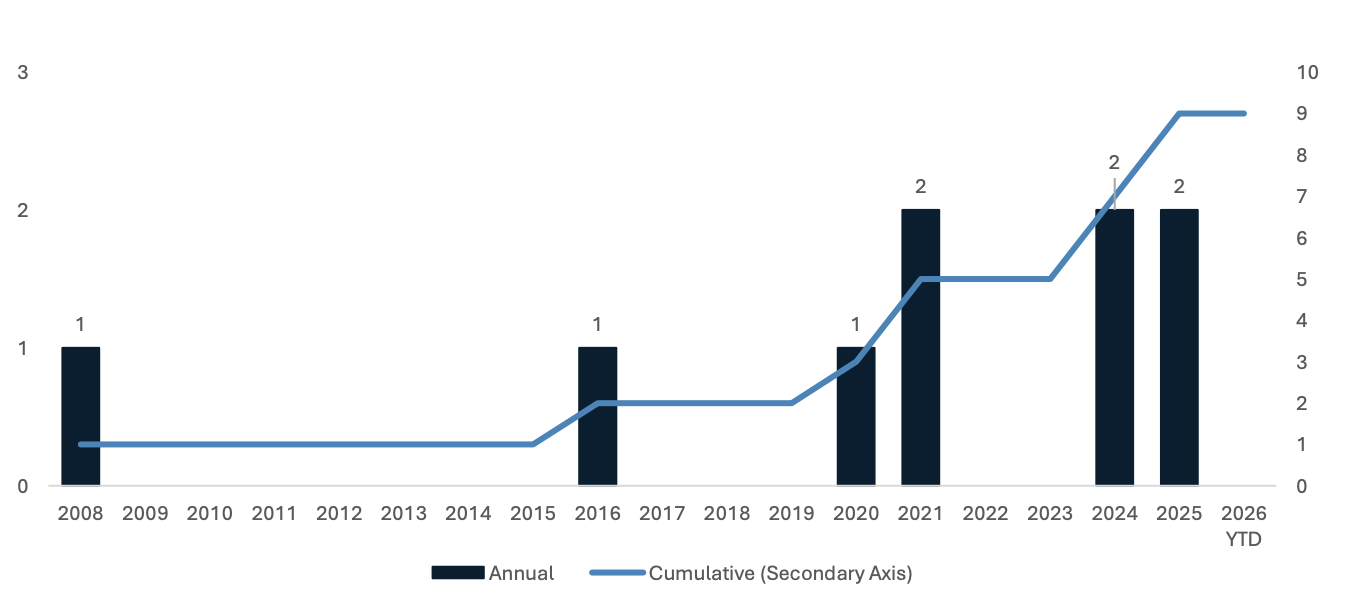

Early liquidity in GP stakes was driven almost entirely by portfolio-level transactions, such as the sale of AMF’s portfolio to Credit Suisse in 2008 and the subsequent sale of Petershill I to Affiliated Managers Group in 2016. Similar to single-investment realizations, portfolio-level transactions have accelerated significantly since 2020, with 7 of 9 total deals occurring in that period and 4 since the start of 2024.

Figure 8: GP Stakes Portfolio Realization Count

In GP stakes, portfolio realizations have historically occurred through three channels: portfolio sales, IPOs and strip sales / continuation vehicles (“CVs”). Prior to 2024, there had not been any meaningful strip sale or CV transaction. Since that date, there have been four announced transactions of this type, which we estimate to comprise more than $4B in value. We believe this demonstrates a continued expansion of GP stakes portfolio liquidity options.

Figure 9: GP Stakes Portfolio Strip Sales / Continuation Vehicles

These transactions involve selling a vertical, pro rata slice of fund economics to an external buyer or GP-sponsored continuation vehicle. Sponsor relationships with the GP stakes investor remain unchanged; however, new LPs may join and holding periods are realigned. Given their demonstrated success and accelerating adoption, we expect these structures to be a continuing source of portfolio liquidity in GP stakes.

Comparative Dynamics by Fund Size

GP stakes liquidity options exist across all fund sizes, however we are likely to see different themes evolve. Single-investment IPOs are likely to remain more prevalent among larger sponsors, given the typical scale required to access public markets. For remaining single-investment and portfolio liquidity options, we believe the mid-market provides more flexibility. We believe this is for three reasons.

Prevalence of Control M&A

Among single-investment realizations, control M&A has been the most frequent liquidity source to-date. While certain large control acquisitions generate the most headlines (e.g., Blackrock’s acquisitions of GIP or HPS), the majority of control activity over the past decade has been among sponsors in our targeted universe. By our analysis, since 2021, acquired GPs have a median AUM of $4.2 billion and average AUM of $13.4 billion. For a mid-market GP stakes investor targeting firms with $1-10B in FPAUM, this falls within the expected range of a targeted sponsor’s size once an investment matures.

Potential for Sponsor-to-Sponsor Sales

In addition, the most recent developing single-investment liquidity route has been sponsor-to-sponsor sales. As in other private equity strategies, we are witnessing the development of an ecosystem within which a mid-market investor can be the first institutional owner of an asset and ultimately sell that investment to a larger investor following the achievement of key value creation initiatives.

Benefits of Scale in Portfolio Monetization

Lastly, as it pertains to portfolio monetization, larger size can present a challenge. The historical examples for full portfolio monetization (Asset Management Finance and Petershill I) have both pertained to smaller portfolios. As GP stakes funds become very large, a substantial monetization becomes more challenging. Even a successful multi-billion-dollar transaction may only monetize a comparatively small portion of a large fund’s portfolio.

Conclusion

GP stakes is often misperceived as illiquid, due to its relative youth and longer hold periods. As the strategy has matured, realization activity has accelerated—at both the single-investment and portfolio level. Monetization events, alongside organic distributions and portfolio financings, create multiple sources of liquidity. As a result, despite longer targeted hold periods, GP stakes funds consistently deliver elevated DPI to their investors. With each realization, a virtuous cycle appears to be forming: exits reinforces investor confidence in the strategy, which in turn supports additional capital flows and further enhances liquidity across GP stakes.

1. Data excludes continuation vehicles established during the same period.